Kaul, however, was unfazed. “‘During demonetisation, you said cash will die. During covid-19, you said cash is dying. How many times will it die,’ I asked them,” he told Mint during a recent interaction in his office in Mumbai.

However, that wasn’t the response the investors were looking for. But Kaul, a former chief executive of Microsoft India, had something more to offer. “Perception is bigger than reality. We told the investors they would be gaining entry into a new business, one that we have spent money on from our books. If it scales up they would see the gains,” he said. Kaul was referring to remote monitoring, a business that entails overseeing automated teller machines (ATM) remotely to prevent unauthorized transactions.

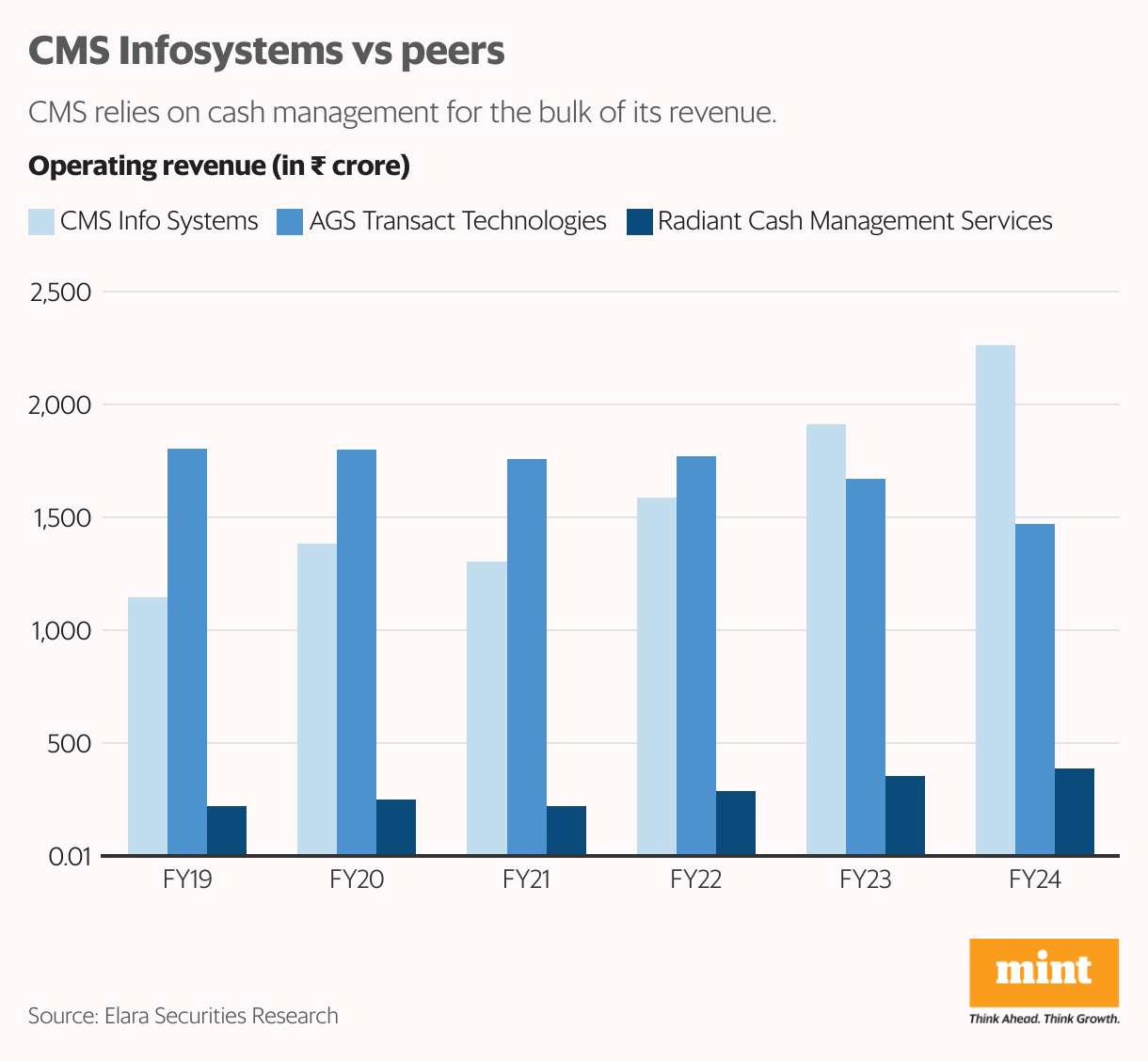

The investors’ concern is understandable. For years, CMS, a company that went public in December 2021, has relied on cash management for the bulk of its revenue. Even today, 62.5% of its top line comes from cash management. But, with the threat from digital payments looming large, the company has started to diversify into new lines of business. Aside from remote monitoring, it is now looking to get into debt collection and bullion logistics.

The company’s financials indicate that it isn’t in any immediate danger. CMS clocked revenue of ₹2,265 crore in FY24 and it is targeting a topline of ₹2,500-2,700 crore this fiscal year. The company’s consolidated net profit stood at ₹347 crore in FY24, having risen steadily from ₹168.5 crore in FY21.

But in the years since Kaul’s meeting, while cash usage has not declined, the explosion in digital transactions has remained a worry for CMS’s investors. There has been a staggering 90-fold increase in retail digital payments over the past 12 years. The country now accounts for nearly half (46%) of the digital transactions in the world, global consultancy PwC said in its India Payments Handbook, released in August, citing data from the Reserve Bank of India (RBI).

In particular, since its launch in August 2016, the Unified Payments Interface (UPI) has unleashed a digital payments revolution in India, clocking more than 10 billion transactions a month since August 2023. Indeed, the number of transactions had shot up to 16.6 billion in October.

While all these statistics have put India on the map for all the right reasons, they’re not music to the ears if you’re working at CMS. And Kaul, who has been associated with the company for nearly 17 years, has his task cut out as he leads the overhaul to future-proof the company from the onslaught of digital payments.

Looking beyond cash

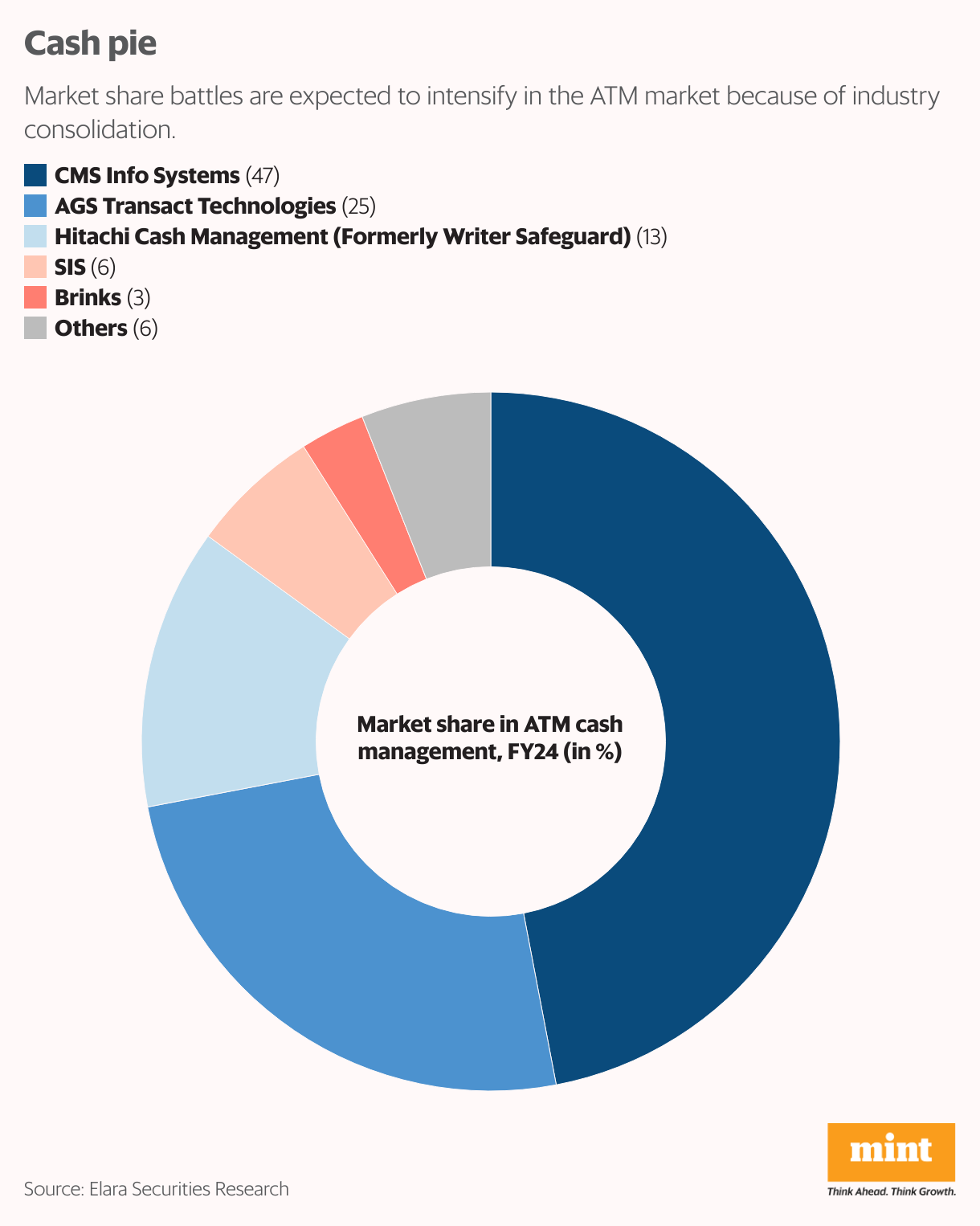

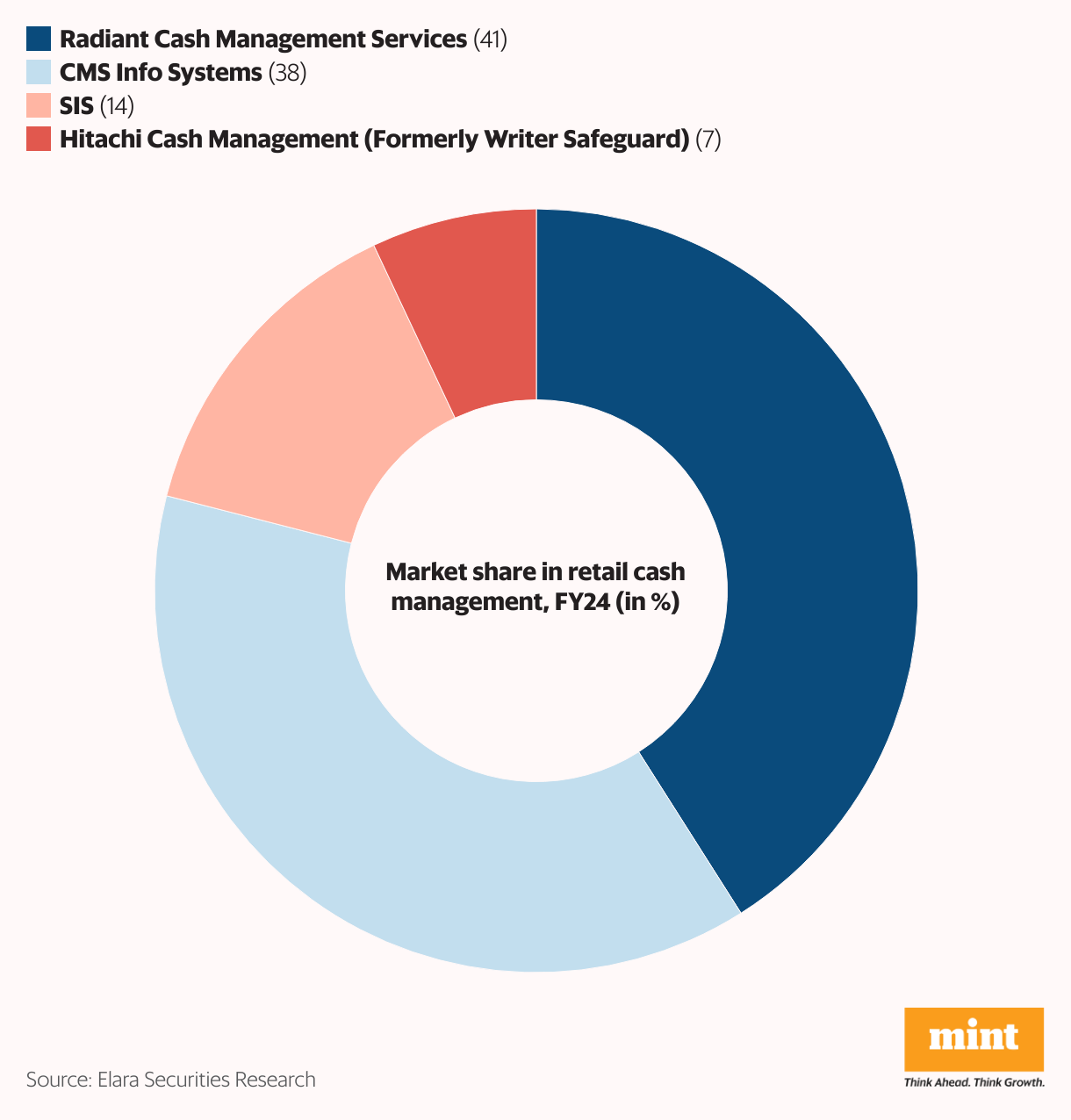

CMS offers cash management, managed services, and other services (which include issuing credit and debit cards for banks). In the first segment, it manages cash at ATMs and also provides vans to transport currency to and from branches. The company’s competitors in this line of business include AGS Transact, Brinks, SIS Prosegur, and Radiant Cash Management. It also has a retail cash management service, under which it offers cash pick-up and delivery solutions to retailers.

Managed services include sale and maintenance of ATMs to banks, setting up and managing brown-label ATMs (where the ATM is managed by a third-party in the bank’s name), providing software solutions for ATMs, and, of late, remote monitoring of ATMs. Rivals here include Diebold Nixdorf, Euronet, FIS, FSS, and Hitachi Payments.

When it comes to diversification, Kaul and his team are betting big on the payback from remote monitoring of ATMs. In March 2022, CMS acquired Hemabh Technology to enter the business.

Remote monitoring entails keeping an eye out for unusual activity at ATMs from a centralized monitoring centre. CMS uses artificial intelligence (AI) and video analytics to look at ATM camera feeds to detect intrusions, vibrations, glass breaks, smoke, and so on. Having a “comprehensive e-surveillance mechanism”, as envisaged by an RBI circular from June 2019, reduces the need for banks to have a security guard at ATMs.

In a note on 7 October, analysts at Elara Securities said that the untapped potential in the remote monitoring space is huge, given that over 60% of ATMs and bank branches are not on AIoT (artificial intelligence of things) solutions. “As the legacy base of ATMs is under a refresh cycle, there is a potential to cross-sell this solution to private banks or public sector banks,” the report said.

Other analysts are also watching the monitoring business with interest, with Jefferies pegging the total market at ₹6,000-9,000 crore across ATM, bank and NBFC branches, telecom towers, retail stores and quick commerce, besides others. The brokerage noted that CMS will face competition from Indian as well as foreign entities, but said its integrated platform, competitive cost of implementation, and regulator-led demand for such implementation is helping the market. “From India, its competitors are iVIS, Igzy, Securens, Modern Informatics, SIS, Zicom, Boparai etc. and international players are Honeywell, Johnson Controls, Hitachi, Eagle Eye, among others,” it said in a note to clients on 3 June.

Bullion logistics involves last-mile deliveries to jewellery stores, traders and bullion companies, while thedebtcollection business will involve collecting repayments on behalf of non-bank financial companies.Among other things, it will include managing the call centre, having feet on the street to execute collection, and carrying out background data analytics to help the frontline staff. Both these businesses were incubated in FY25.

The firm does not want to get into bad-loan recovery and risk sullying its reputation as the business involves different pressure tactics.

— Rajiv Kaul

“Last year, we invested almost $1 million to incubate the collection business, get clients and get experience,” said Kaul. CMS is now looking for partners to scale up this business. That said, there are some lines that Kaul does not want to cross. There are two kinds of collections in the market, he noted, one where loans are overdue for up to 90 days and another where loans have turned bad and repayments are long pending. The company does not want to get into bad-loan recovery and risk sullying its reputation as the business involves “different pressure tactics”, he explained.

Debt collection has earned a bad name in recent years because of the strong arm tactics of agents on the ground. In September 2022, for instance, the RBI had asked Mahindra & Mahindra Financial Services (Mahindra Finance) to stop recoveries through external agencies after the alleged death of an individual in the process. The restrictions were lifted four months later.

“Given that the RBI is hassled about NBFC collection practices, we thought the sector would get regulated over time. Just for NBFCs, it is a ₹25,000-30,000 crore total addressable market,” said Kaul, indicating why CMS has chosen this business to diversify.

Early days

In its initial years, CMS, which was founded by Ramesh Grover and others in 1976, was an IT infrastructure management company that, among other things, provided traffic management services.

In 2008, private equity giant Blackstone partnered with the CMS Group to set up a new company, carving out IT infrastructure management, ATM cash management, and other businesses. In a statement that December, Blackstone said it owned a majority stake in this new company and had inked an agreement with Kaul to lead it.

")

View Full Image

A few years into the acquisition, Kaul started shrinking the number of business segments. “The first year and a half, we did not have enough money to pay salaries and hire a senior team. We hived off the IT infrastructure maintenance business and others since we realised that these would not reach market leadership.”

They focused their energies on building the cash management business. “None of us knew anything about that business (when we bought CMS). I had no clue, but we made it India’s biggest. Then we used it to build the transformation that CMS is going through,” said Kaul.

In 2015, Baring Asia bought the entire company (CMS Info Systems) from Blackstone and the Grover family for ₹2,000 crore. Under Baring, CMS made six acquisitions. The private equity firm finally exited in February, after selling stakes over multiple tranches since CMS’s 2021 public offering. Currently, the company does not have a promoter and is wholly owned by public shareholders, which include mutual funds, alternative investment funds, foreign portfolio investors, and Kaul, among others.

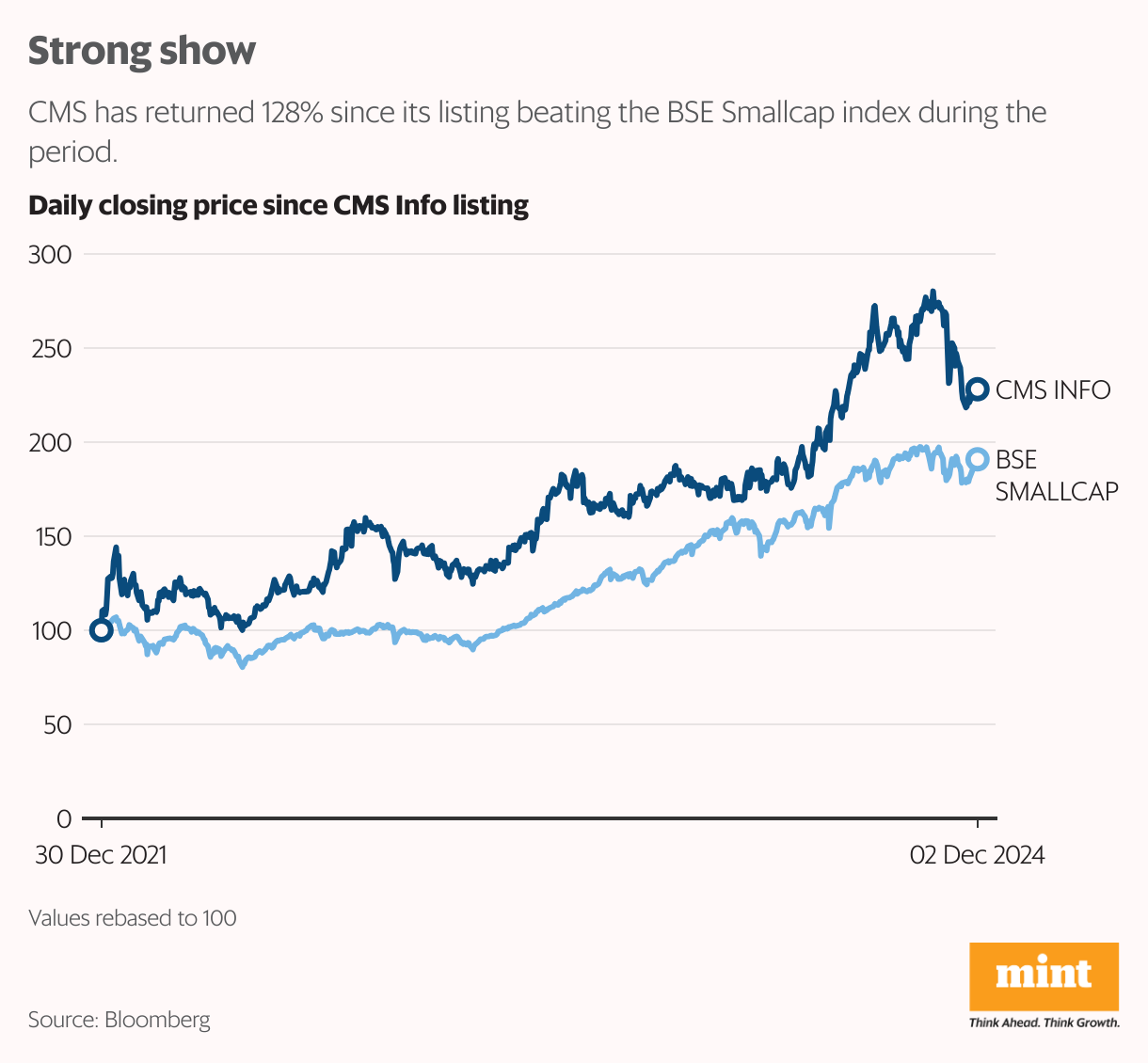

Over the past year, the CMS stock has gained 24.2% on the BSE, as compared to a 34.5% rise on the broader BSE Smallcap index, of which it is a part.

Positive expectations

Analysts are quite upbeat about CMS’ plans, given that it reduces the company’s reliance on cash for revenue. In a note on 28 October, Jeffries said that as diversification in (the) non-cash market plays out, it sees potential for a rerating.

Others are counting on NBFCs and banks viewing the outsourcing of secondary activities favourably. “We believe that banks and NBFCs will look to adopt leaner models by outsourcing non-core activities, and CMS Info Systems is well-positioned to support this shift given its robust execution record, experienced leadership, scalable solutions, and pan-India presence,” Elara Securities said in its 7 October note, while initiating coverage on the company.

Another positive for CMS is that while digital payments may seem like a dark cloud, the silver lining is the amount of cash in the system, which has only grown—cash is still very much the king in India.

Currency in circulation stood at ₹35.6 trillion as on 15 November, per RBI data, up from ₹33.6 trillion on 17 November 2023. The level is nearly double of what it was during demonetisation in November 2016, when high-value currency notes were declared invalid overnight.

Another positive for CMS is that while digital payments may seem like a dark cloud, the silver lining is the amount of cash in the system, which has only grown—cash is still very much the king in India.

Explaining the phenomenon, Bhavik Hathi, managing director, Alvarez and Marsal, said that assuming India’s GDP is growing at 6-7%, it would mean that business volumes would also be growing at the same rate and cash in circulation would also increase after accounting for digital adoption. “Overall digital adoption is not at par with the pace at which India is growing, thereby leading to more cash being needed,” he said. “At least in the next decade, I do not see the position of cash in the system changing dramatically. There will be an inflection point but, it is difficult to predict when that will come.”

Challenges aplenty

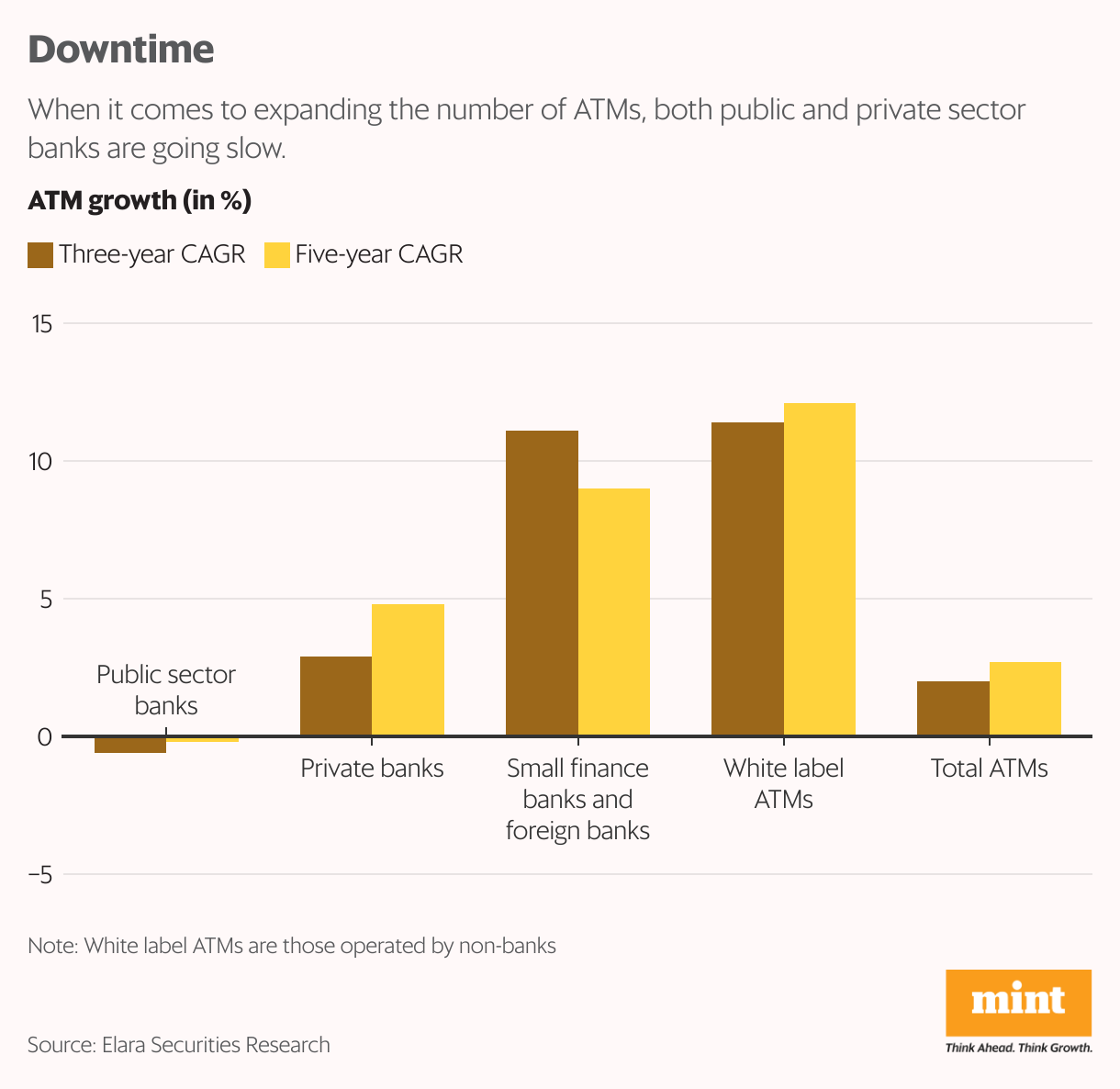

Despite its diversification strategy, given that the primary business still involves cash, which accounts for 60% of its revenue, CMS has to depend on banks expanding their ATM networks and people using cash as a medium to purchase goods and services.

With digital payments becoming ubiquitous, banks have gone slow on expanding the number of ATMs. In fact, between October 2023 and October 2024(the latest available monthly data), ATMs and cash recycling machines of public, private, foreign banks and small finance banks declined 2% to216,208, as per data from the RBI. The total ATM base of state-owned banks and private sector banks has shrunk 1.7% and 1.5%, respectively, over the same period.

In the ATM space, analysts also see a threat to CMS Info Systems’s market share in the wake of Hitachi Payment Services, the Indian arm of Japanese multinational Hitachi, acquiring Writer Corporation’s cash management business in January. Hitachi Payment Services did not have a cash logistics business and banks have been usingthe services of CMS or other competitorsfor the same, while the Japanese subsidiary handled other aspects of cash management. In the wake of the recent acquisition, banks could now potentially give the whole service contract to Hitachi.

And despite the enthusiasm around new businesses at CMS, analysts believe there is an execution risk. “The inability to maintain efficiency in operations could hit margins and thus create value. (There is also a) risk from new entrants: Loss in market share driven by competitive pricing from new entrants may risk valuations,” said the Elara Securities note cited earlier.

Acknowledging the risks, Kaul emphasized that the management will focus on profitability while looking to diversify. The idea is to be the market leader in any business CMS targets, but not by spending to achieve scale.